Posts

Building a decision tree algorithm from scratch

Building a decision tree from scratch Sometimes to truly understand and internalise an algorithm, it’s always useful to build from scratch. Rather than relying on a module or library written by someone else.

I’m fortunate to be given the chance to do it in 1 of my assignments for decision trees.

From this exercise, I had to rely on my knowledge on recursion, binary trees (in-order traversal) and object oriented programming.

Martingale Strategy - Double Down

Martingale Strategy In this post, I will simulate a martingale strategy in Roulette’s context to highlight the potential risks associated with this strategy.

Double down! That’s essentially the essence of it.

Here’s a simple explanation of the strategy,

The croupier spins the ball. If it’s red you win the amount you bet, black you lose the same amount If you win, you continue to bet the same amount (same as your 1st bet amount) If you lose, you double your bet amount And if your accumulated winnings hits a certain amount, you stop and leave the casino So how would the strategy fare?

How to Create a Python Environment in Ubuntu or any Debian-based system

Often, certain projects or classes involving python require a set of modules/packages for the code to work.

1 solution is to create a Python Environment dedicated to that project.

First set up a folder, and include a .yml file with the specific modules and environment that you wish to install. Here is an example (env.yml),

name: env channels: !!python/tuple - !!python/unicode 'defaults' dependencies: - nb_conda=2.2.0=py27_0 - python=2.7.13=0 - cycler=0.10.0 - functools32=3.

Translating Ernest Chan Kalman Filter Strategy Matlab and Python Code Into R

Translating Ernest Chan Kalman Filter Strategy Matlab and Python Code Into R I’m really intrigued by Ernest Chan’s approach in Quant Trading.

Often in the retail trading space, what ‘gurus’ preach often sounds really dubious. But Ernest Chan is different. He’s sincere, down-to-earth and earnest (meant to be a pun here).

In my first month of deploying algo trading strategies, I focus mainly on mean-reversion strategies - paricularly amongst pairs.

How I Find Country Pairs for Mean Reversion Strategy

How I Find Country Pairs for Mean Reversion Strategy As mentioned in my previous post here, the first step for a mean reversion strategy is to conduct some background quantitative research.

Step 1 First, I use a pair trading function to loop across 800+ country pairs (created from combination function),

pair_trading = function(stock1, stock2, trade_amount, finance_rates, start_date, end_date, prop_train, enter_z_score, exit_z_score){ ## More codes here ## Return this key_info = list( ticker = c(stock1, stock2), start_date = start_date, trade_table = data_trade, sharpe = c(sharpeRatioTrainset, sharpeRatioTestset), half_life = half_life, profits = data_trade_stats, max_drawdown = c(table.

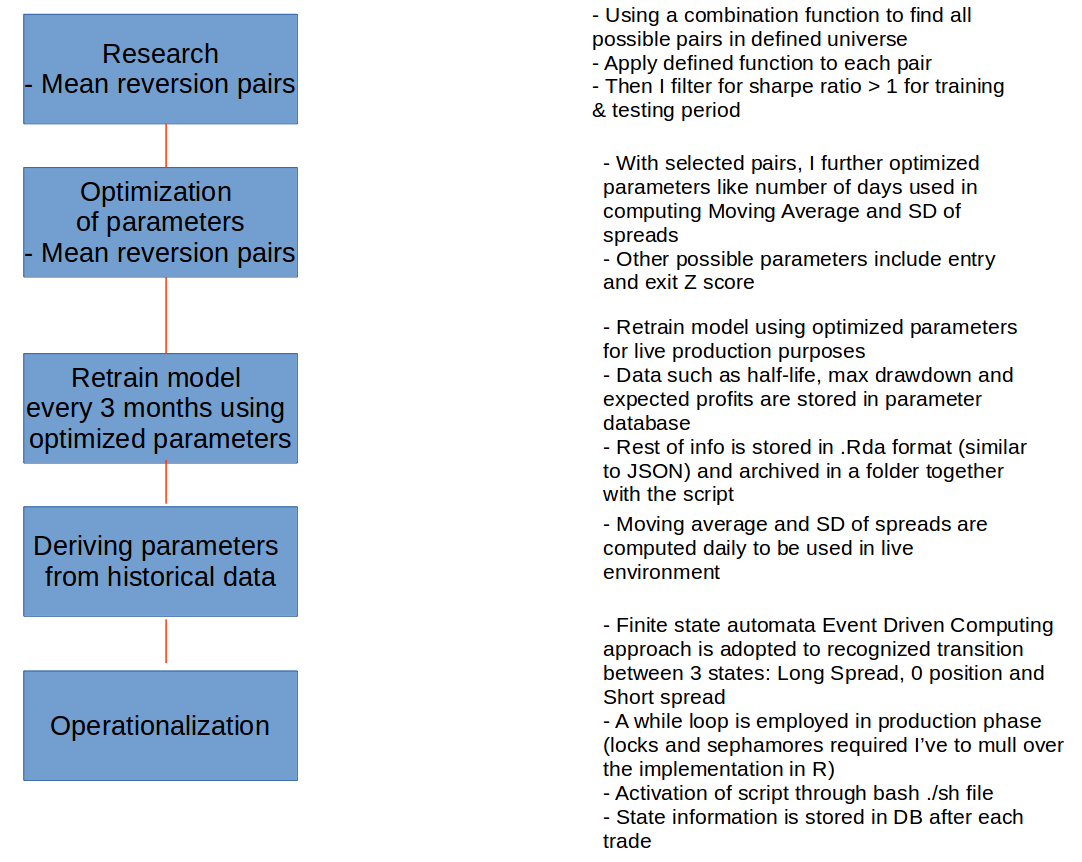

Research to Production Pipeline for Mean Reversion

Research to Production Pipeline for Mean Reversion

Here is a high level overview of something that I’m working on.

I’ve been grappling with the finite state automata Event Driven Computing transitions and I kinda sorted it out for production use.

Prototype Pair Trading Strategy for Silver ETFs

In these 2 weeks, I’ll deploy my pair trading algo strategy into my server.

I modified the code below from a renowned quant trader, Ernest Chan. The basic idea is to find z-scores through moving average & moving SD of spread. If it’s more than absolute of z-score, I will either short or long the spread depending on the polarity.

In the backtesting below (using a pair of silver ETFs as an example), I assumed a hypothetical amount of 10,000 dollars per trade.

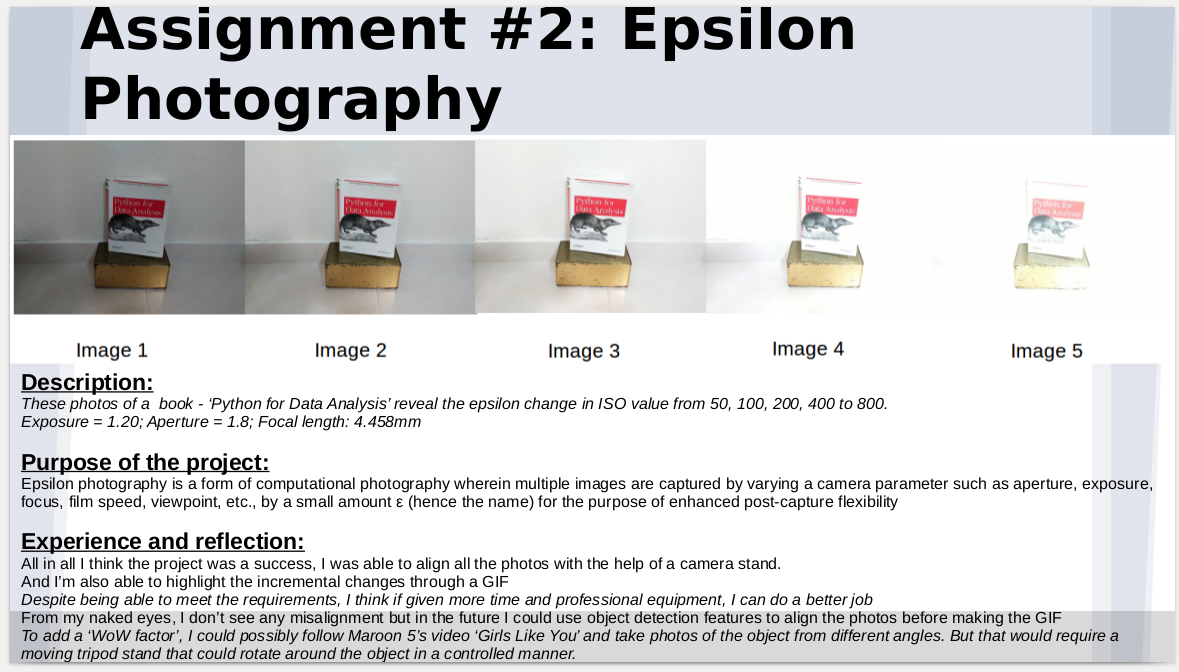

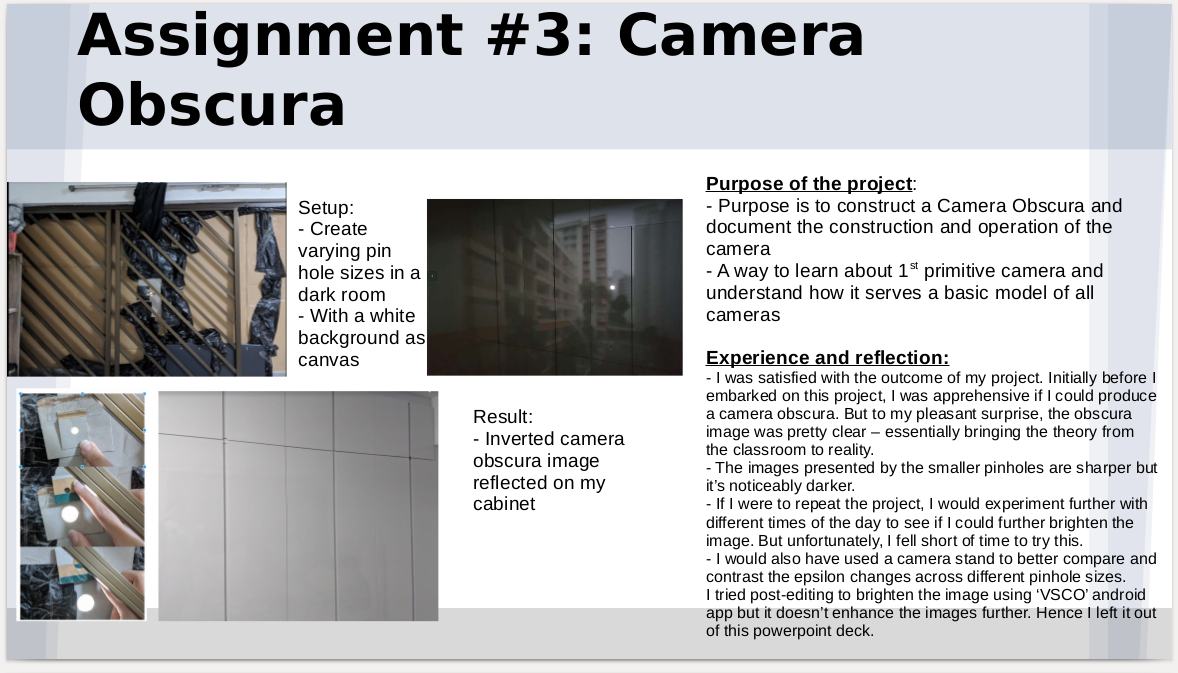

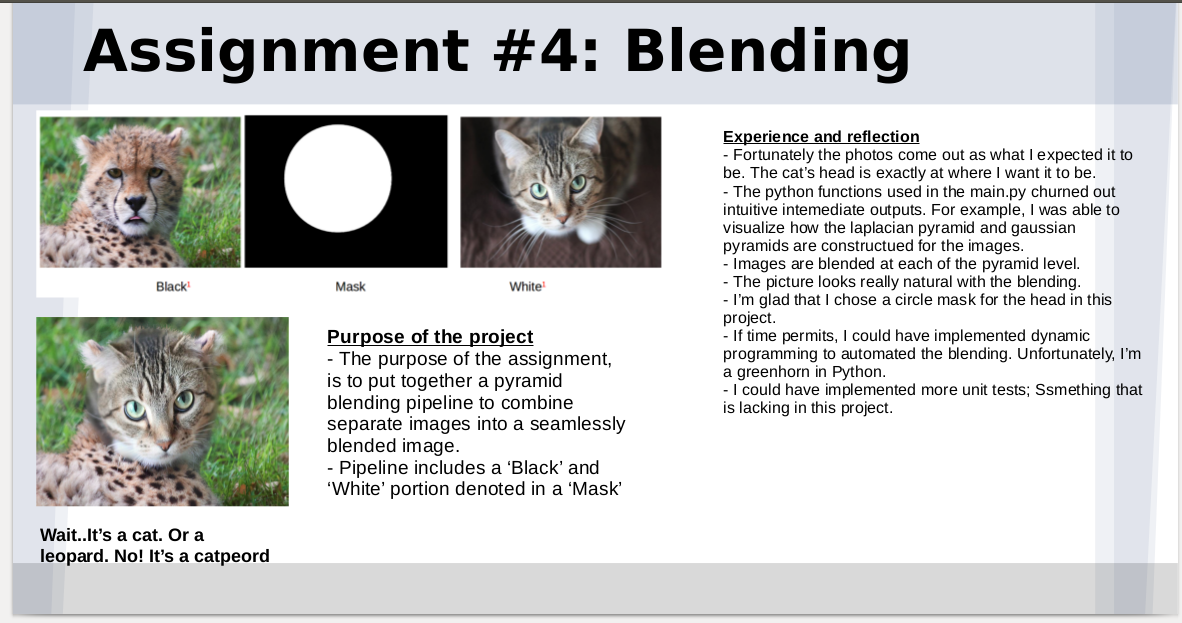

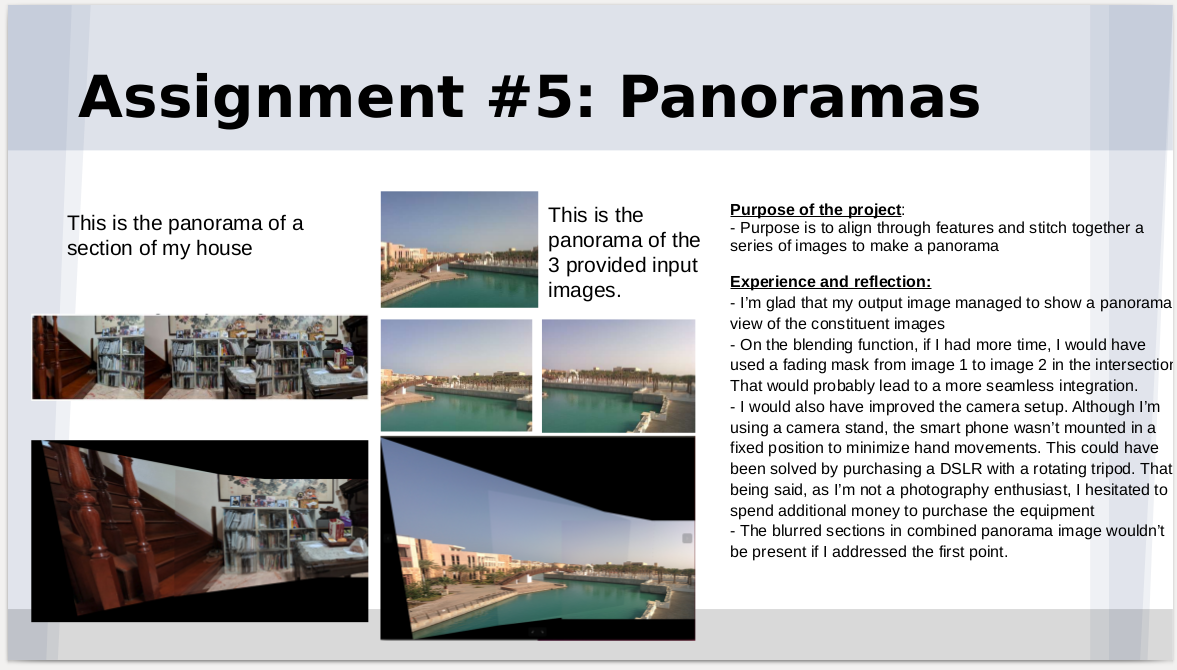

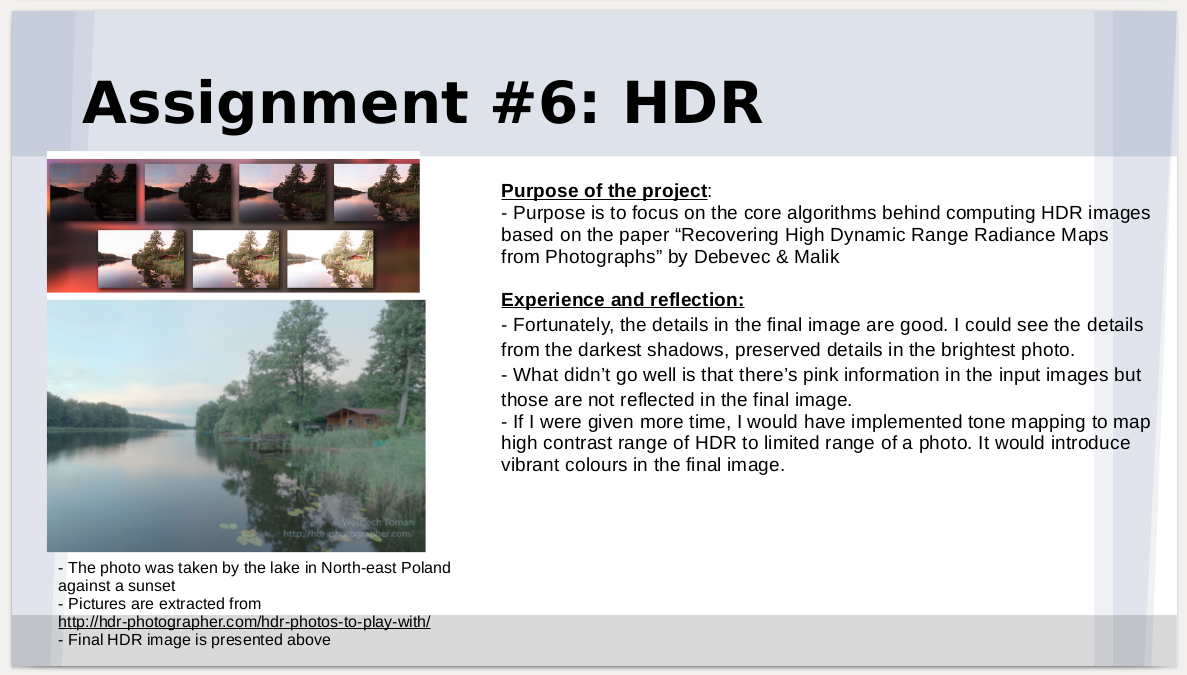

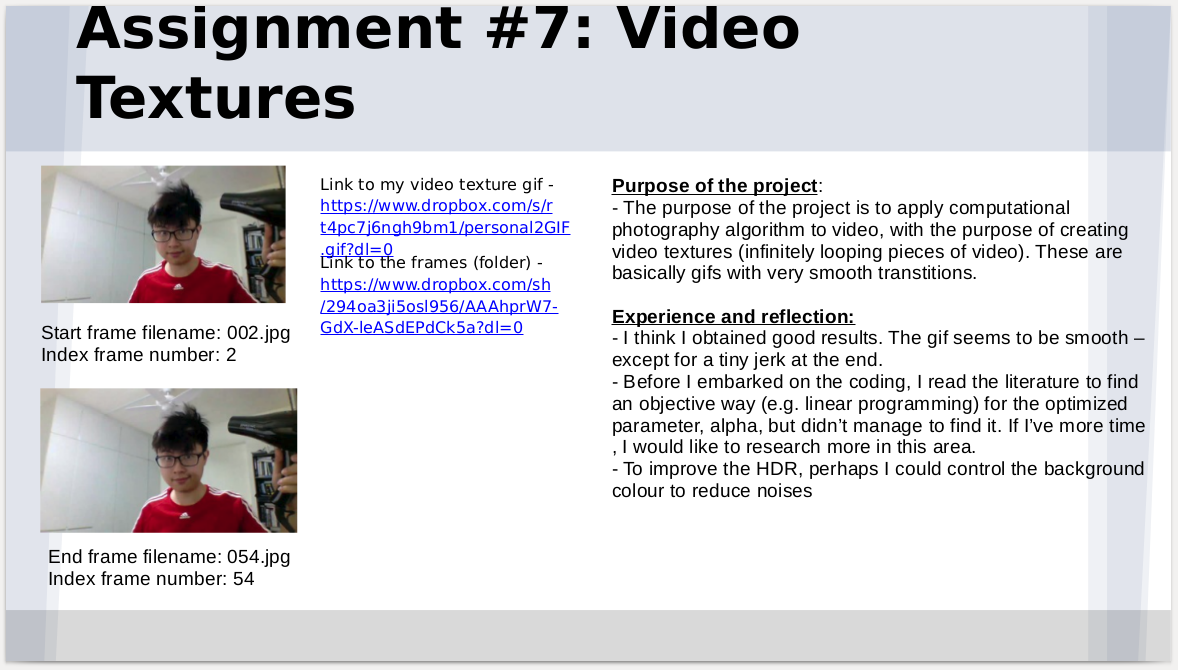

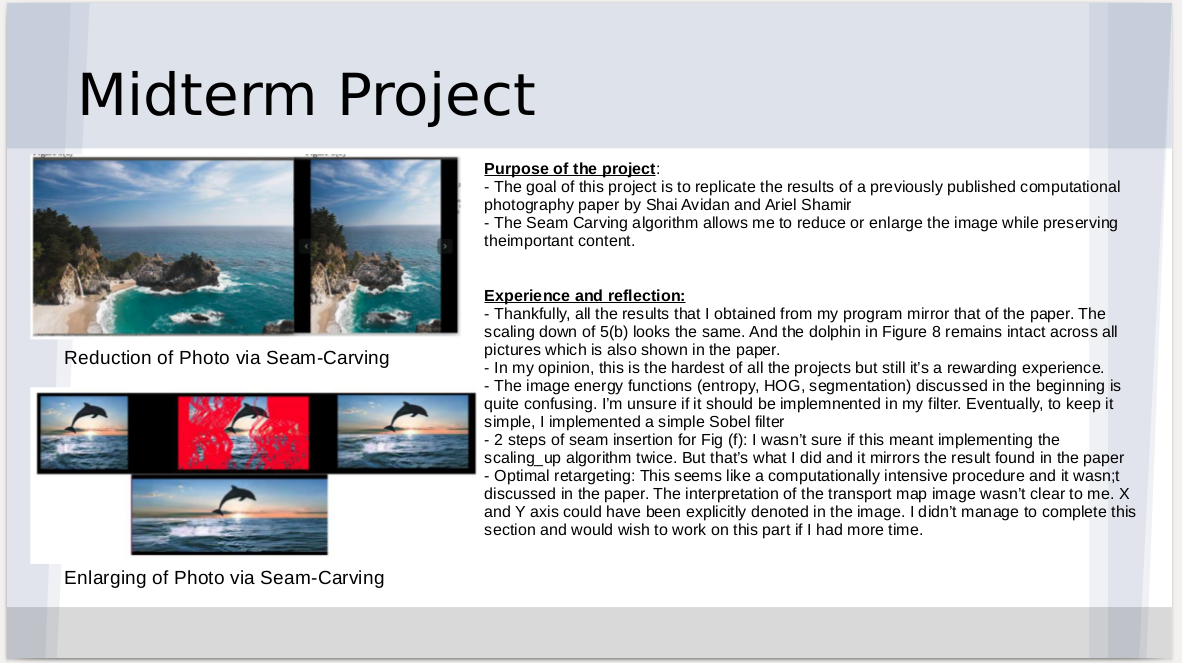

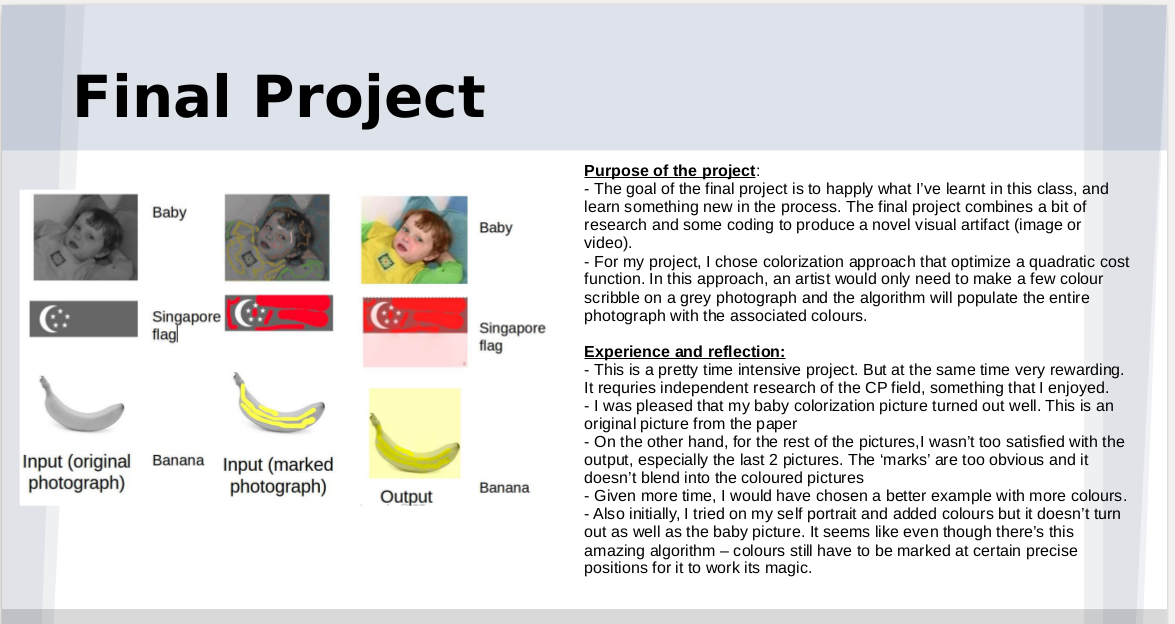

Summary of My Computational Photography Module From Georgia Tech Computer Science Masters

For what’s worth, here is a summary of what I went through for my Georgia Tech Computer Science Msc Computational Photography module.

And it’s really painful but rewarding!

Colorization

Colorization The following is a high level project pipeline of my Computational Photography Colorization report. The project scope involves minimizing a quadratic cost function. An artist would only need to make a few colour scribble on a grey photograph and the algorithm will automatically populate the entire photograph with the associated colours.

1.Input: I first read in the image using imread function.

2.Find the difference: Next I compute the difference between the marked and grey scale image.

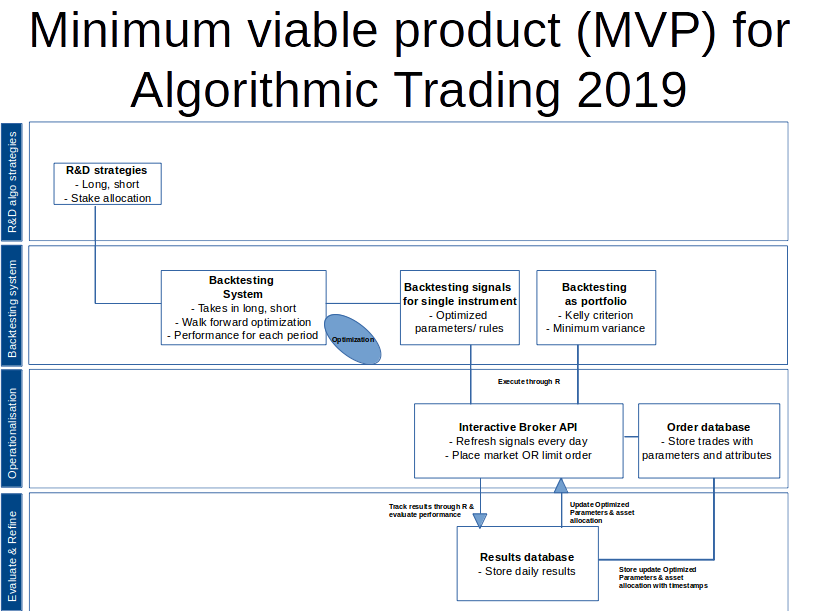

Architecture and Process Flow for My Algorithmic Trading

Project that I will be working in 2018-2019