Decomposing a Position Into Exchange Rate and Non Exchange Rate Effects

If you are someone with a stake in foreign positions, this package I wrote here may be a useful tool to help you understand the impact of foreign currency on your positions. For instance,

- If you are an investor, you may use it to analyze impact of exchange rate on your investment positions.

- If you are in the treasury department, you may wish to analyze the impact of exchange rates on your bonds.

- If you are in the finance department, you could analyze the exchange rate impact on your foreign revenue.

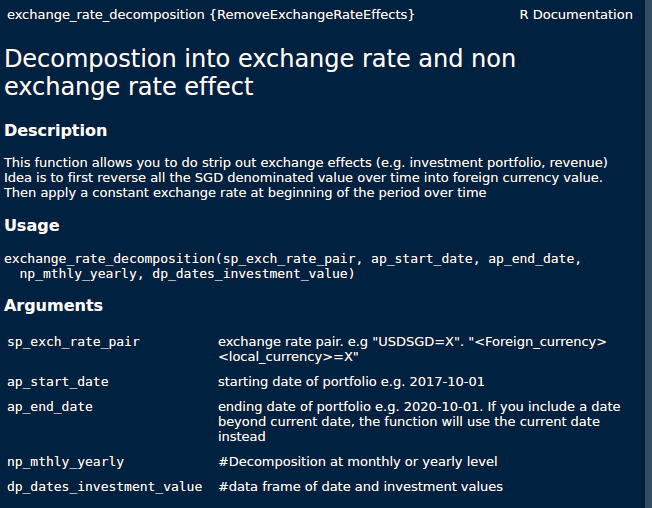

To start using this package, you may first install the devtools package and execute the following command. install_github(“jironghuang/RemoveExchangeRateEffects”). The R documentation is as follows,

You may follow the 2 examples to better understand how this package works.

Example 1

In summary, what the example does below is to decompose 1 instrument position in SGD (column value) - from the perspective of someone staying in Singapore - into local static value (i.e if I keep the exchange rate constant at the start of the period) and the residual exchange rate impact.

If you look at the value at the end of the period (Oct 2018), you would notice that the value in SGD fell from 331 to 261. From the perspective of a Singaporean local - through this package - we can understand that the appreciation in USD negate the fall in value by 4 SGD.

If you are an economist, you could have considered the exchange rate elasticities. But let’s ignore that for now.

Quick example 1 in R codes (decomposing a single instrument)

library(devtools)

install_github("jironghuang/RemoveExchangeRateEffects")

library(RemoveExchangeRateEffects)

sp_exch_rate_pair = "USDSGD=X" #exchange rate pair. e.g "USDSGD=X". "<Foreign_currency><local_currency>=X"

ap_start_date <- as.Date("2017-10-01") #starting date of portfolio e.g. 2017-10-01

ap_end_date <- as.Date("2020-10-01") #ending date of portfolio e.g. 2020-10-01. If you include a date beyond current date, the function will use the current date instead

np_mthly_yearly = "monthly" #alternatively this could be "yearly""

data(eg_dat) #example dataset that I included in this package

dp_dates_investment_value = instrument

o_exchRate_effect <- exchange_rate_decomposition(sp_exch_rate_pair, ap_start_date, ap_end_date, np_mthly_yearly, dp_dates_investment_value)

o_exchRate_effect$get_portfolio()

value_in_sgd exchange_rate fgn_value local_static_value exch_rate_impact

Oct 2017 331.53 1.36010 243.7541 331.5300 0.0000000

Nov 2017 308.85 1.34670 229.3384 311.9231 -3.0731344

Dec 2017 311.35 1.33780 232.7328 316.5399 -5.1899425

Jan 2018 354.31 1.31168 270.1192 367.3892 -13.0791734

Feb 2018 343.06 1.32433 259.0442 352.3260 -9.2660108

Mar 2018 266.13 1.31090 203.0132 276.1183 -9.9882495

Apr 2018 293.90 1.32577 221.6825 301.5104 -7.6103599

May 2018 284.73 1.33850 212.7232 289.3248 -4.5948212

Jun 2018 342.95 1.36830 250.6395 340.8948 2.0552438

Jul 2018 298.14 1.36140 218.9952 297.8553 0.2846937

Aug 2018 301.66 1.36700 220.6730 300.1374 1.5226438

Sep 2018 264.77 1.36732 193.6416 263.3719 1.3980921

Oct 2018 260.95 1.38061 189.0107 257.0734 3.8766087

o_exchRate_effect$get_diff_portfolio_value()

[1] 3.8766087

Example 2

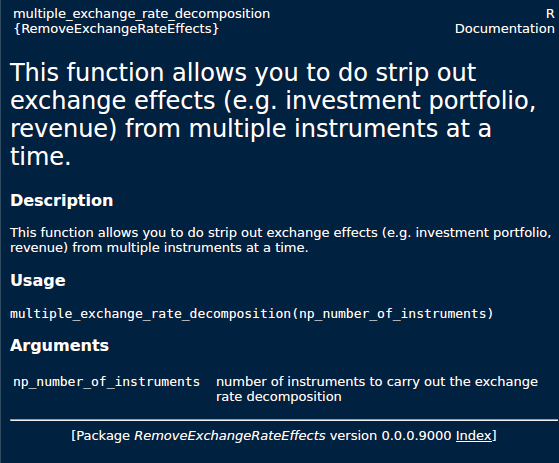

The second example builds upon the first. I’ve expanded the previous function to decompose multiple instruments at once.

get_full_decomposition() returns a list of data frames with the decompositions.

But before you implement the function above, you would have to add the information via the mutator functions as shown in the example below (the functions with the prefix set)

Quick example 2 in R codes (Decomposing multiple instruments at 1 time)

data(eg_dat)

er = c("USDSGD=X", "GBPSGD=X")

start_date = c("2017-10-01", "2017-10-01")

end_date = c("2020-10-01", "2020-10-01")

freq = c("monthly", "monthly")

dat = list(eg_dat, eg_dat)

o_exchRate_effect <- multiple_exchange_rate_decomposition(2)

o_exchRate_effect$set_sa_exch_rate_pair(er) #adding an array of exchange rate pairs

o_exchRate_effect$set_sa_start_date(start_date) #adding an array of starting dates

o_exchRate_effect$set_sa_end_date(end_date) #adding an array of ending dates

o_exchRate_effect$set_sa_mthly_yearly(freq) #adding an array of "monthly" or "yearly" option

o_exchRate_effect$set_dl_dates_investment_value(dat) #adding list of data frames

o_exchRate_effect$get_full_decomposition() #carry out decomposition and obtain a list of data frames

[[1]]

value exchange_rate fgn_value local_static_value exch_rate_impact

Oct 2017 331.53 1.36010 243.7541 331.5300 0.0000000

Nov 2017 308.85 1.34670 229.3384 311.9231 -3.0731344

Dec 2017 311.35 1.33780 232.7328 316.5399 -5.1899425

Jan 2018 354.31 1.31168 270.1192 367.3892 -13.0791734

Feb 2018 343.06 1.32433 259.0442 352.3260 -9.2660108

Mar 2018 266.13 1.31090 203.0132 276.1183 -9.9882495

Apr 2018 293.90 1.32577 221.6825 301.5104 -7.6103599

May 2018 284.73 1.33850 212.7232 289.3248 -4.5948212

Jun 2018 342.95 1.36830 250.6395 340.8948 2.0552438

Jul 2018 298.14 1.36140 218.9952 297.8553 0.2846937

Aug 2018 301.66 1.36700 220.6730 300.1374 1.5226438

Sep 2018 264.77 1.36732 193.6416 263.3719 1.3980921

Oct 2018 260.95 1.38061 189.0107 257.0734 3.8766087

[[2]]

value exchange_rate fgn_value local_static_value exch_rate_impact

Oct 2017 331.53 1.79703 184.4877 331.5300 0.0000000

Nov 2017 308.85 1.80690 170.9281 307.1629 1.6870605

Dec 2017 311.35 1.79812 173.1531 311.1613 0.1887369

Jan 2018 354.31 1.85680 190.8175 342.9048 11.4051640

Feb 2018 343.06 1.84162 186.2816 334.7537 8.3062984

Mar 2018 266.13 1.83911 144.7059 260.0408 6.0892228

Apr 2018 293.90 1.82588 160.9635 289.2562 4.6437963

May 2018 284.73 1.77878 160.0704 287.6513 -2.9212846

Jun 2018 342.95 1.78907 191.6918 344.4759 -1.5258666

Jul 2018 298.14 1.78638 166.8962 299.9175 -1.7774444

Aug 2018 301.66 1.77860 169.6053 304.7858 -3.1258259

Sep 2018 264.77 1.78285 148.5094 266.8759 -2.1058633

Oct 2018 260.95 1.76900 147.5127 265.0848 -4.1347817